Most California founders spend more energy naming their company than choosing its legal structure. That's an expensive mistake. The california startup legal structure explained correctly is not just about picking LLC, S Corp, or C Corp from a dropdown. It's about understanding that your legal structure and your tax classification are two separate decisions, and confusing them can cost you thousands in avoidable fees before you even open your doors. This guide breaks down both layers clearly, so you can make a decision grounded in real numbers rather than guesswork.

Table of Contents

- Key takeaways

- California startup legal structures: what each entity actually means

- Tax classification vs. legal structure: where founders go wrong

- Real cost comparison: LLC vs. S Corp vs. C Corp in California

- Compliance, investor expectations, and scaling your structure

- My take on the one mistake that defines most California startup stories

- How Legalstepz can help you get this right from day one

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Legal structure ≠ tax classification | Choosing an LLC or corporation only sets your legal form; IRS tax elections determine how you're taxed. |

| California franchise tax hits every entity | LLCs, S Corps, and C Corps all owe California franchise tax, with rates and minimums that vary significantly. |

| S-Corp election has a hard deadline | You must file Form 2553 by March 15 for calendar-year taxpayers or risk defaulting to a higher tax rate. |

| Delaware C-Corp doesn't escape California taxes | Foreign qualification still triggers California franchise tax and compliance obligations if you operate here. |

| Compliance calendars aren't optional | Missing IRS or California state deadlines can cost you your preferred tax status entirely. |

California startup legal structures: what each entity actually means

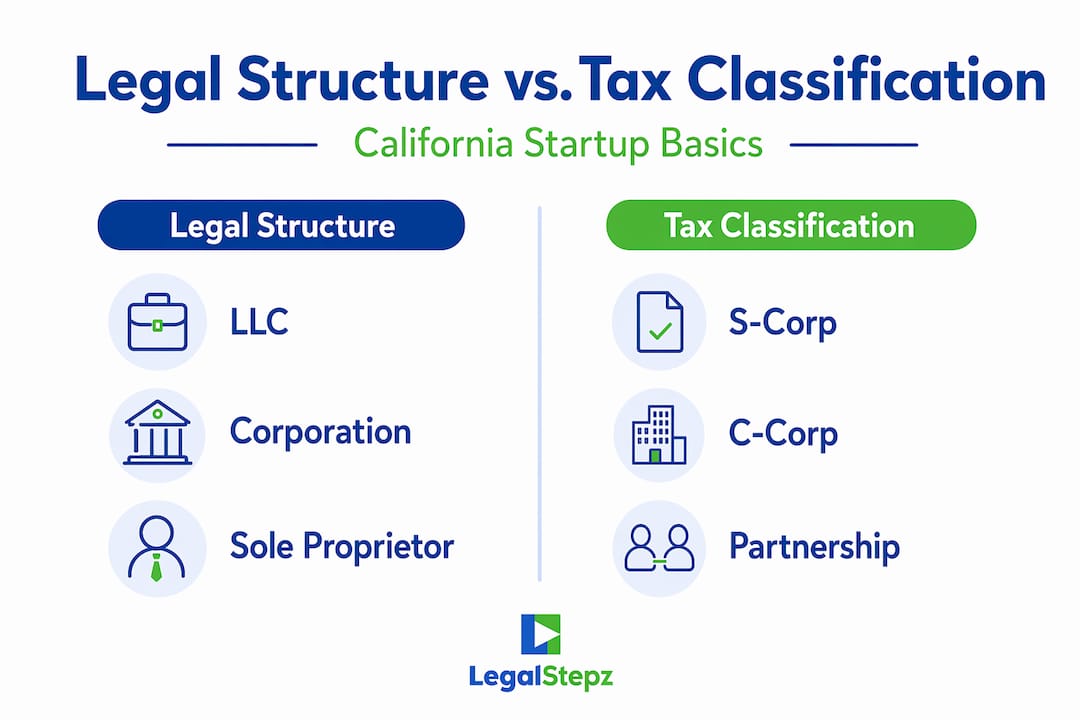

Before you can make a smart choice, you need a clear picture of your options. There are four primary entity types in California: LLC, S Corporation, C Corporation, and sole proprietorship. Each creates a different legal relationship between you, your business, and its debts.

A sole proprietorship is the simplest form. No formation paperwork, no separation between you and the business. If the business gets sued, you get sued personally. Most serious startups move past this quickly.

An LLC (Limited Liability Company) creates a separate legal entity that shields your personal assets from business liabilities. It's flexible, relatively affordable to maintain, and popular with early-stage founders. By default, the IRS taxes a single-member LLC like a sole proprietorship and a multi-member LLC like a partnership. Neither classification is automatically the most tax-efficient.

A C Corporation is its own legal and tax entity. It pays corporate income tax, and shareholders pay tax again on dividends. This double-taxation sounds bad, but the structure has specific advantages, especially for venture-backed companies that plan to raise institutional capital.

An S Corporation is a tax classification, not a standalone legal structure. You form a corporation or LLC first, then elect S-Corp status with the IRS. That distinction matters more than most founders realize.

Here's a quick reference for the four structures:

| Entity type | Personal liability protection | Default federal tax treatment | California franchise tax |

|---|---|---|---|

| Sole proprietorship | None | Schedule C (personal return) | None (but note: not applicable) |

| LLC | Yes | Disregarded/partnership | $800 minimum + gross receipts fees |

| S Corporation | Yes | Pass-through to owners | 1.5% of net income |

| C Corporation | Yes | Corporate rate (21%) | 8.84% of net income |

The table above shows why entity choice is more than a legal formality. The tax rates attached to each structure in California create real cost differences that compound over time.

Tax classification vs. legal structure: where founders go wrong

This is where the costly confusion starts. When you form an LLC, you have created a legal structure. You have not automatically chosen the most advantageous tax classification.

The IRS allows LLC owners to elect how they want to be taxed through two forms. Form 8832 lets you elect corporate tax treatment for your LLC. Form 2553 elects S-Corp tax treatment, and filing Part IV of Form 2553 automatically reclassifies your LLC to a corporation for tax purposes, which means you don't need to file Form 8832 separately.

The S-Corp election is particularly powerful for profitable California startups, but it comes with timing rules most founders underestimate. The IRS deadline is March 15 for calendar-year taxpayers who want the election to apply to that tax year. Miss it, and your business defaults to pass-through LLC or standard C-Corp tax treatment for the entire year. Late election relief is available in some cases (up to 3 years and 75 days with reasonable cause), but relying on that is risky.

California adds another layer. The state recognizes your federal S-Corp election, but you must also file Form 100S annually with the California Franchise Tax Board. Fail to file correctly, and California taxes you at the C-Corp rate of 8.84% instead of the 1.5% S-Corp rate.

Key compliance facts to track:

- IRS Form 2553 must be filed no later than 2 months and 15 days after the start of the tax year you want the election to take effect

- California does not have a separate S-Corp election form; it follows your federal election automatically

- California Form 100S must be filed annually to maintain the 1.5% franchise tax rate

- LLC gross receipts fees stack on top of the $800 minimum, regardless of profitability

Pro Tip: Set your S-Corp election deadline on your compliance calendar the day you form your entity. Treating the election as an afterthought is the number-one reason founders end up paying the wrong tax rate for an entire year.

Real cost comparison: LLC vs. S Corp vs. C Corp in California

Numbers make this concrete. Let's say your startup clears $150,000 in profit in year two.

As a default LLC, you pay 15.3% self-employment tax on the full amount (federal), plus income tax, plus California's $800 minimum franchise tax and applicable gross receipts fees. LLC owners pay SE tax on every dollar of profit, with no way to split income into salary versus distributions.

Under S-Corp election, you pay yourself a reasonable salary (say, $80,000), and that's the only amount subject to self-employment tax. The remaining $70,000 flows to you as a distribution, free of SE tax. California charges 1.5% franchise tax on net income rather than the LLC fee schedule. At higher profit levels, the savings compound fast. At $350,000 profit, the franchise tax difference between a C Corp and an S Corp alone exceeds $25,000 per year.

C-Corps pay a flat 21% federal corporate rate and California's 8.84% franchise tax. The double-taxation problem becomes real when you distribute profits as dividends. However, if your startup is retaining earnings to fund growth or anticipates a venture capital raise, the C-Corp math can work in your favor.

One often-overlooked option: California's AB 150 Pass-Through Entity tax election allows qualifying S Corps and LLCs to pay state tax at the entity level and then claim a federal credit. This effectively bypasses the $10,000 SALT deduction cap and can save several thousand dollars annually for the right businesses.

Pro Tip: Run your tax comparison at two profit levels: where you are now and where you expect to be in three years. The entity that saves you money at $80,000 in profit may cost you at $300,000.

When a C-Corp earns its place:

- You plan to raise institutional capital from venture firms

- You want to issue multiple classes of stock (S-Corps are limited to one class)

- You plan to offer employee stock option plans (ESOP)

- Your exit strategy involves an acquisition or IPO

Compliance, investor expectations, and scaling your structure

Entity choice is not a one-time decision. It's a strategy that should evolve with your business. This is why California entrepreneurs need a compliance calendar, not just a formation checklist.

Here's a practical sequence for getting this right from the start:

- Choose your legal structure based on liability needs, funding plans, and operational complexity.

- Make your tax election within the IRS deadline window. Don't wait until tax season.

- File California-specific forms to align your state tax classification with your federal election.

- Set annual compliance reminders for Statement of Information filings, franchise tax payments, and annual minutes.

- Revisit your structure annually as revenue grows and investor conversations evolve.

On the investor side, most institutional venture capital firms expect a Delaware C-Corp. Delaware's corporate law is well-established, its courts are predictable, and investors and their lawyers know the documents. If you incorporate in California instead, some term sheets will require you to reincorporate before closing.

Here's the trap many founders miss: incorporating in Delaware doesn't eliminate your California tax obligations. If you operate here, you must register as a foreign corporation in California, pay California franchise tax, and maintain compliance filings in both states. You don't escape California. You add a second state.

Pro Tip: A California startup document organization guide sounds boring until you're scrambling to find your original bylaws or meeting minutes during a due diligence request. Create a dedicated folder structure from day one: formation documents, annual filings, tax elections, and board minutes each get their own section.

For ongoing annual requirements, maintaining limited liability means keeping up with filings, meeting minutes, and registered agent obligations. These aren't just bureaucratic boxes. Courts have pierced the corporate veil and held founders personally liable for business debts when proper records weren't kept.

My take on the one mistake that defines most California startup stories

I've watched founders spend $5,000 on brand identity work and $200 on their entity formation. Then they call a tax professional at year-end and discover they defaulted into a structure that cost them $12,000 more than it needed to. That pattern repeats more than it should.

The thing I keep coming back to is this: entity choice is a living strategy, not a checkbox at formation. Most guides treat it as a one-time administrative task, but it's actually the first financial decision you make on behalf of your company. Made wrong, it compounds every year.

The S-Corp election is where I've seen the most expensive mistakes. Founders learn about the self-employment tax savings from a podcast or a thread online. They form an LLC and assume the election happens automatically. It doesn't. The deadline passes unnoticed, and they pay full SE tax for another year. The savings they planned their financial model around never arrive.

California's franchise tax is equally misunderstood. I've spoken with founders who incorporated in Delaware specifically to avoid California taxes. They were surprised to learn that operating in California still triggers full franchise tax obligations. The geography of your operations, not your state of incorporation, determines your California tax exposure.

My honest advice: treat your entity choice and your compliance calendar as the same conversation. Neither works without the other.

— Peter

How Legalstepz can help you get this right from day one

Getting your entity structure right in California requires more than reading articles. You need the right documents filed correctly, annual obligations tracked, and compliance maintained year after year.

Legalstepz offers practical tools and courses built specifically for California entrepreneurs. Whether you're forming an LLC and working through the LLC formation process for the first time, or incorporating and preparing your bylaws and annual minutes, Legalstepz gives you step-by-step guidance tailored to California's specific requirements. From registered agent services to Statement of Information filings, the platform handles the compliance pieces that trip up most early-stage founders. Start your entity on the right legal and tax foundation at Legalstepz.com.

FAQ

What is the difference between a legal structure and a tax classification?

Your legal structure (LLC, corporation) determines liability protection and formation requirements. Your tax classification (sole proprietor, partnership, S-Corp, C-Corp) determines how the IRS and California tax your income. These are separate decisions.

When do I need to file Form 2553 for S-Corp status in California?

The IRS requires Form 2553 to be filed no later than 2 months and 15 days into the tax year you want the election to apply. For calendar-year businesses, that deadline is March 15.

Does incorporating in Delaware avoid California franchise tax?

No. If your startup operates in California, you must register as a foreign corporation and pay California franchise tax regardless of where you incorporated.

Which entity type do venture capital investors prefer?

Most institutional investors expect a Delaware C-Corp. Delaware's legal framework and investor familiarity make it the standard for VC-backed startups, even with the added California compliance costs.

What is the California AB 150 Pass-Through Entity tax election?

AB 150 lets qualifying S Corps and LLCs pay California income tax at the entity level and claim a federal credit, effectively working around the $10,000 federal SALT deduction cap to reduce total tax liability.