Mixing your personal and business finances is one of the fastest ways to create accounting headaches, tax problems, and legal exposure. When you open a business bank account in California, you build a clean financial foundation that makes bookkeeping simpler, tax time less painful, and your business look legitimate to clients and vendors. California has specific documentation requirements that vary by business structure, and walking into a bank unprepared can cost you days or weeks of delays. This guide walks you through every step, from gathering documents to choosing the right bank for your needs.

Table of Contents

- Key takeaways

- How to open a business bank account in California: what you need first

- The step-by-step process for opening your account

- Common challenges and what to do about them

- Top California business banking options

- My honest take after years of watching this process

- Get your business formation right before you bank

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Documents vary by structure | LLCs, corporations, and sole proprietors each need different formation documents to open an account. |

| EIN speeds everything up | Getting your Employer Identification Number online takes minutes and unlocks most bank applications. |

| Preparation prevents delays | Matching your documents to your bank's requirements before you apply cuts onboarding time significantly. |

| Multi-member LLCs face extra steps | Beneficial ownership reporting under the 2026 Corporate Transparency Act adds documentation requirements. |

| FDIC limits matter for larger deposits | Standard coverage caps at $250,000, but some fintech options extend protection well beyond that. |

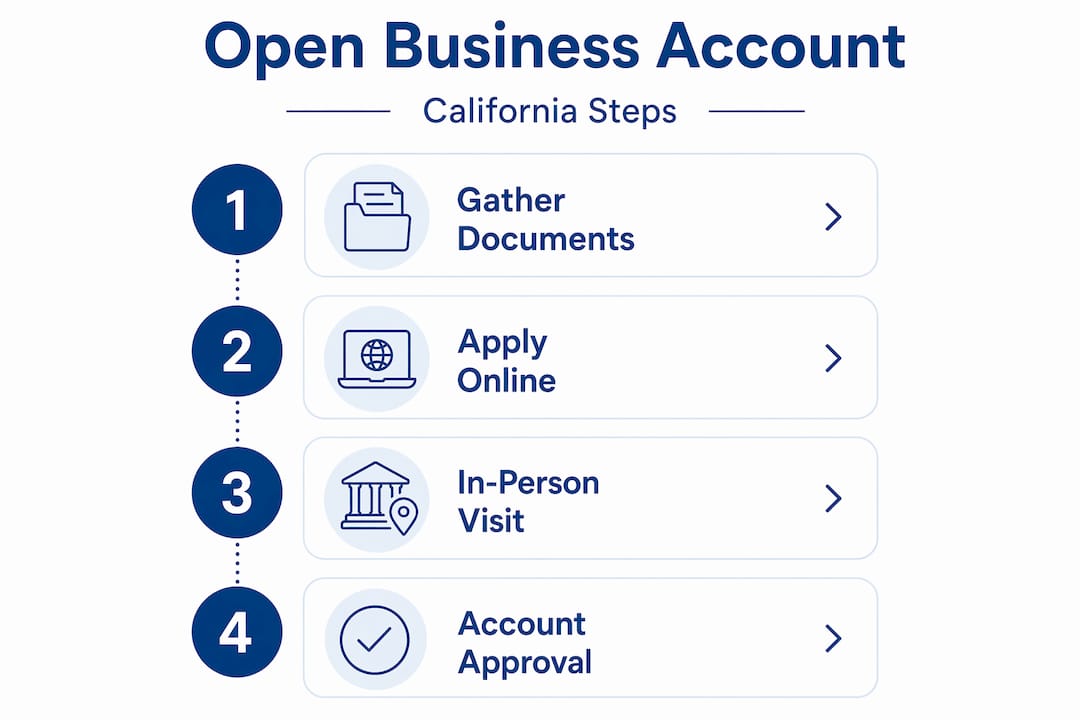

How to open a business bank account in California: what you need first

Before you fill out a single application, you need to gather the right documents. Banks run identity and compliance checks on every new business account, and missing or mismatched documents can cause outright denials or weeks of back-and-forth. What you need depends almost entirely on your business structure.

Documents by business type

Here is what California banks typically require based on entity type:

- Sole proprietor: Government-issued photo ID, Social Security Number or EIN, and a DBA (Doing Business As) certificate if you operate under a trade name. You can file a DBA with your county clerk's office.

- Single-member LLC: Articles of Organization filed with the California Secretary of State, your EIN, and a government-issued ID. Some banks also ask for your California Statement of Information.

- Multi-member LLC: Everything above, plus your operating agreement and personal identification for every member who owns 25% or more. Beneficial ownership data is now required under the 2026 Corporate Transparency Act, so have that information ready.

- Corporation: Certificate of Incorporation, corporate bylaws, a board resolution authorizing the account, and your EIN.

Your EIN is the single most important number in this process. Banks use it to verify your tax identity, and most will not open a business account without one. The IRS online EIN application issues your number in minutes, and it costs nothing. You can only submit one application per day, so do not wait until the morning of your bank appointment.

Pro Tip: If you formed a California LLC, pull your Articles of Organization directly from the California Secretary of State's website before your appointment. Banks want the stamped, filed version, not a draft.

For a detailed walkthrough on forming a California LLC or getting your EIN for an LLC, Legalstepz has step-by-step guides that cover both processes in plain language.

| Business Structure | Key Documents Needed |

|---|---|

| Sole Proprietor | Photo ID, SSN or EIN, DBA certificate (if applicable) |

| Single-Member LLC | Articles of Organization, EIN, photo ID |

| Multi-Member LLC | Articles of Organization, operating agreement, EIN, IDs for all 25%+ owners |

| Corporation | Certificate of Incorporation, bylaws, board resolution, EIN |

The step-by-step process for opening your account

Once your documents are in order, the actual account opening is straightforward. Here is how to move through it without wasting time.

- Choose your bank. Think about branch access, monthly fees, transaction limits, and digital tools. If you deposit cash regularly, a bank with California branches matters. If your business is fully online, a fintech with no fees may serve you better.

- Decide: online or in person. Many banks let you apply digitally or at a branch. Online applications work well for simpler structures like sole proprietors and single-member LLCs. Multi-member LLCs and corporations often need to visit a branch because of the additional identity verification involved.

- Submit your documents. Upload or bring your formation documents, EIN confirmation letter, and IDs. Banks run a Customer Identification Program (CIP) check, which verifies both the business and the people behind it.

- Make your opening deposit. Most business checking accounts require a minimum deposit to activate. This ranges from $0 at some fintechs to $100 or more at traditional banks. Ask about this before you apply.

- Select your account type. A business checking account handles day-to-day transactions. A business savings account holds reserves. If you accept card payments, ask about merchant services accounts too.

- Confirm activation. After approval, make a small test transaction and log into online banking to verify everything works before you start routing client payments.

Pro Tip: Bring one extra copy of every document to your branch appointment. Banks sometimes need to make copies, and having extras prevents a second trip.

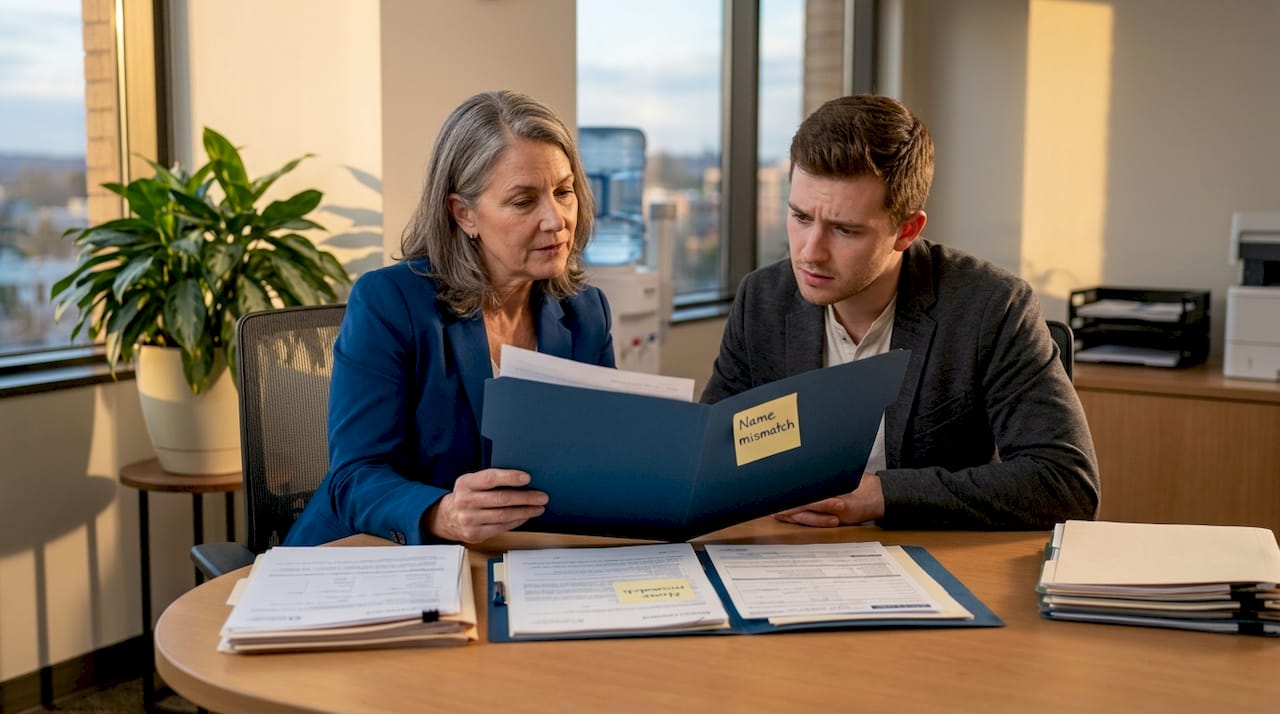

The biggest pitfall at this stage is showing up with documents that do not match. For example, if your LLC is registered under one name but your DBA is under another, the bank's compliance team will flag it. Preparing correct documents upfront dramatically shortens onboarding time.

Common challenges and what to do about them

Even with good preparation, you may hit a few snags. Knowing what they are ahead of time means you can resolve them quickly instead of starting over.

Document mismatches are the most common reason applications stall. If your Articles of Organization list a registered agent address that differs from your operating address, some banks will ask for clarification. Always review your formation documents for consistency before applying.

Multi-member LLC complexity is real. Under 2026 regulations, operating agreements must clearly define who the authorized signers are. If your agreement is vague, the bank may require all members to appear in person to open the account. Updating your operating agreement before you apply prevents this entirely.

FDIC insurance limits are worth understanding, especially if your business holds significant cash reserves. Standard FDIC coverage caps at $250,000 per depositor per bank. Some fintech platforms use sweep networks to extend that protection. Bluevine's program insures funds up to $3 million by distributing deposits across multiple FDIC-insured partner banks. If your business regularly holds more than $250,000 in cash, this is worth factoring into your bank choice.

Commingling personal and business funds can invalidate your LLC's liability protection, exposing you personally to business debts. A dedicated business account is not optional for LLC owners. It is the structural firewall that makes your LLC actually work.

Once your account is active, add authorized signers carefully. Each signer typically needs to appear in person with valid ID. Keep your account in good standing by maintaining any required minimum balances and staying current with your annual filings, including your California Statement of Information.

Top California business banking options

Choosing where to bank matters as much as how you open the account. Here is a practical look at your main options.

| Bank / Fintech | Best For | Monthly Fee | FDIC Coverage |

|---|---|---|---|

| Chase | Branch access, lending | $15 (waivable) | $250,000 standard |

| Bank of America | Nationwide presence | $16 (waivable) | $250,000 standard |

| U.S. Bank | Midwest/West Coast presence | $0 to $25 | $250,000 standard |

| Bluevine | Online businesses, high FDIC | $0 | Up to $3 million |

| Live Oak Bank | Industry-specific lending | $0 | $250,000 standard |

Chase has hundreds of California branches, which makes it a strong pick if you regularly deposit cash or want face-to-face service. Bank of America offers a similar footprint with solid digital tools. U.S. Bank has a strong presence across the West Coast and works well for businesses that want a mid-size bank feel without the big-bank fees.

For businesses that operate primarily online, fintechs like Bluevine offer no monthly fees and significantly higher FDIC protection. Live Oak Bank specializes in SBA lending, which makes it worth considering if you plan to seek financing down the road.

A few things to weigh when making your choice:

- How often do you deposit cash? (Fintechs rarely support cash deposits)

- Do you need a line of credit or SBA loan access?

- How important is in-person service versus mobile banking?

- What are the transaction limits before fees kick in?

My honest take after years of watching this process

I've guided a lot of California entrepreneurs through the business bank account process, and the pattern I see most often is this: people underestimate how much the bank cares about paperwork precision. It is not that banks are difficult. They are running compliance checks that are non-negotiable, and any gap in your documentation creates a flag.

The businesses I've seen get accounts opened fastest are the ones that treated document preparation as a project, not an afterthought. They had their Articles of Organization, EIN confirmation letter, operating agreement, and IDs organized in a folder before they ever contacted a bank. That level of preparation signals to the bank that you run a real, organized business.

One thing I wish more people understood is the multi-member LLC situation. I've seen partnerships where two or three founders show up to open an account, only to discover their operating agreement does not name a managing member or authorized signer. The bank sends them home. Updating that document takes a week. Preventing it takes ten minutes.

My advice on FDIC coverage is also worth stating plainly: if your business holds more than $200,000 in cash at any point, think seriously about where it sits. The standard $250,000 limit feels like plenty until it is not. Sweep networks exist for exactly this reason, and they are underused by small businesses.

— Peter

Get your business formation right before you bank

Getting your formation documents in order is the single biggest factor in how smoothly your bank account opening goes. Legalstepz helps California entrepreneurs handle the paperwork that banks actually need.

Through Legalstepz, you can file your California Statement of Information, get registered agent services, and access formation support that makes sure your documents are accurate before you walk into any bank. The Incorporation Course walks you through the full formation process step by step, so you arrive at your bank appointment with everything in order. No guesswork, no second trips, no delays from missing paperwork.

FAQ

What documents do I need to open a business bank account in California?

You need your EIN, government-issued ID, and formation documents specific to your business structure. LLCs need Articles of Organization, while corporations need a Certificate of Incorporation and board resolution.

Can I open a California business bank account online?

Yes. Many banks and fintechs allow online applications, especially for sole proprietors and single-member LLCs. Multi-member LLCs and corporations often need to visit a branch for identity verification.

How long does the business bank account process take in California?

With all documents ready, online applications can be approved within one to three business days. In-branch applications for simpler structures are often completed the same day.

Do I need an EIN to open a business bank account?

Most banks require an EIN for LLCs and corporations. Sole proprietors can sometimes use their Social Security Number, but an EIN is recommended for privacy and professional reasons.

What are the best banks for business in California?

Chase and Bank of America offer the widest branch networks in California. For online businesses, Bluevine provides no monthly fees and FDIC coverage up to $3 million through its sweep network program.