A limited partnership is a formal business entity that includes at least one general partner with unlimited personal liability and full management control, and at least one limited partner whose liability is capped at their investment. This structure gives entrepreneurs a legal framework to raise capital from passive investors without surrendering operational control. As a pass-through tax entity, an LP avoids the double taxation that corporations face, making it a preferred structure for real estate syndications, private equity funds, and family investment vehicles. If you are deciding how to structure your next venture, understanding the limited partnership definition is the right place to start.

What is a limited partnership and how does it work?

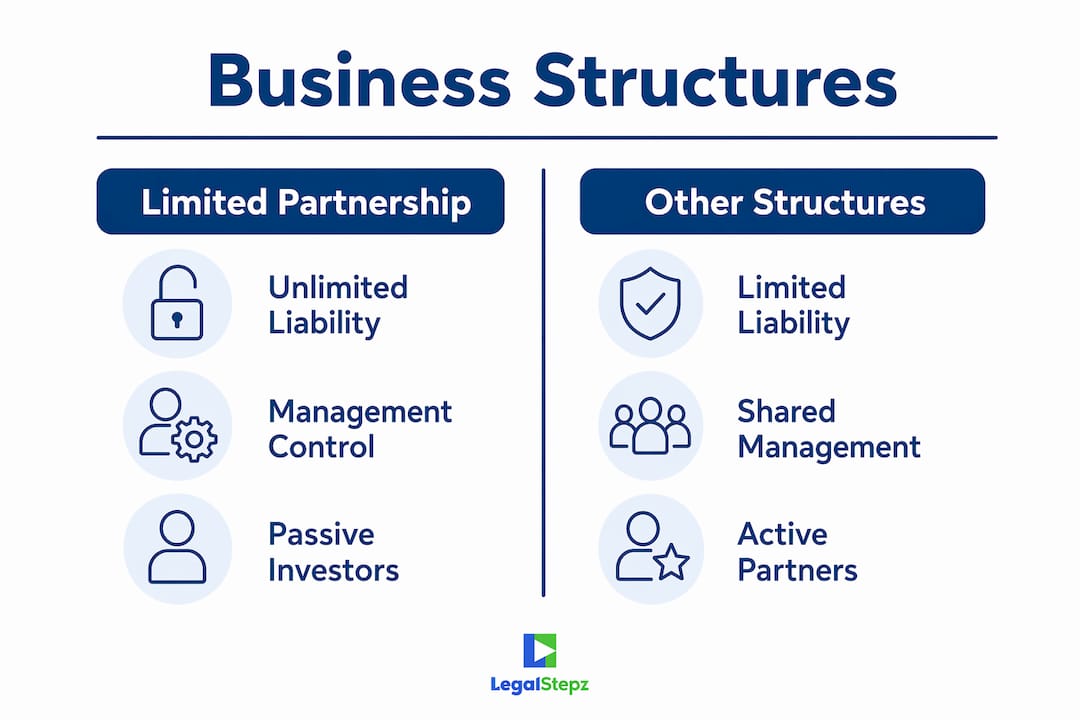

A limited partnership consists of two distinct partner classes, each with different rights, obligations, and exposure. The general partner runs the business, signs contracts, and bears unlimited personal liability for the entity's debts and obligations. The limited partner contributes capital and receives a share of profits but stays out of daily operations. This clean division is what makes the LP structure attractive for capital-intensive ventures.

The general partner's unlimited liability is the trade-off for control. If the LP faces a lawsuit or defaults on a debt, the general partner's personal assets are at risk. Limited partners, by contrast, can only lose what they invested. That asymmetry is the core of the limited partnership definition and the reason investors accept passive roles in exchange for liability protection.

LPs are pass-through entities for tax purposes, meaning profits and losses flow directly to each partner's individual tax return. No tax is paid at the entity level. Limited partners are also generally exempt from self-employment taxes unless they actively participate beyond their investment role. That combination of liability protection and tax efficiency is what draws institutional investors to LP structures.

What are the core roles and responsibilities within a limited partnership?

The general partner and limited partner roles are not interchangeable, and the legal consequences of confusing them are serious.

General partner responsibilities:

- Full management authority over business decisions, contracts, and operations

- Unlimited personal liability for all partnership debts and legal claims

- Fiduciary duty to act in the best interests of all partners

- Responsibility for tax filings, compliance, and annual state reporting

Limited partner responsibilities:

- Capital contribution in exchange for a profit interest

- No participation in day-to-day management or operational decisions

- Liability capped at the amount invested in the partnership

- Rights to inspect financial records and vote on major structural changes

The liability boundary for limited partners is not automatic. Courts may reclassify active limited partners as general partners if they participate in management decisions beyond prescribed safe harbor activities. Safe harbor activities typically include attending meetings, reviewing financial statements, and voting on major transactions. Anything beyond that, such as negotiating contracts or directing employees, creates legal exposure.

One widely used strategy to address the general partner's unlimited liability is forming an LLC as the general partner. The LLC acts as the managing entity, and its members are shielded from personal liability by the LLC's own structure. This approach adds a filing layer but is now considered best practice for entrepreneurs managing LP structures in real estate and private equity.

Pro Tip: Define safe harbor activities explicitly in your limited partnership agreement. A written list of permitted limited partner actions protects both parties and reduces the risk of a court reclassifying a passive investor as a general partner.

How does a limited partnership compare to other business structures?

Many entrepreneurs confuse LPs with limited liability partnerships (LLPs) and general partnerships (GPs). The differences are significant and choosing the wrong structure can create unintended legal exposure.

| Structure | Liability | Management rights | Common use case |

|---|---|---|---|

| Limited partnership (LP) | General partner: unlimited. Limited partner: capped at investment. | General partner controls operations. Limited partners are passive. | Real estate, private equity, family investment funds |

| General partnership (GP) | All partners: unlimited personal liability | All partners share management rights | Small professional practices, informal joint ventures |

| Limited liability partnership (LLP) | All partners: limited liability | All partners may participate in management | Law firms, accounting firms, medical practices |

The LP is the only structure that deliberately separates management from investment. That separation is what makes it the preferred vehicle for institutional investment structures where accountability between operators and capital providers must be clearly defined. The LLP, by contrast, suits professional service firms where all partners contribute expertise and none should bear unlimited risk for another's malpractice.

For entrepreneurs comparing entity structure options, the LP makes the most sense when you need outside capital from passive investors and want to retain full operational control. If your investors want a seat at the management table, an LLC with a detailed operating agreement is likely a better fit.

What are the advantages and disadvantages of forming a limited partnership?

The LP structure offers real benefits, but it also carries constraints that entrepreneurs need to understand before filing.

Advantages:

- Pass-through taxation. Profits and losses are reported on individual returns, avoiding corporate double taxation. This is particularly valuable in real estate, where depreciation deductions pass directly to partners.

- Capital flexibility. LPs are ideal for capital-intensive ventures like private equity and real estate syndications because they allow entrepreneurs to bring in multiple passive investors without diluting management control.

- Liability protection for investors. Limited partners risk only their invested capital, which makes it easier to attract outside funding from individuals who want financial exposure without operational risk.

- Waterfall distribution frameworks. LPs support structured profit-sharing arrangements that allocate returns to investors and managers in a defined sequence, which is a standard feature in real estate and fund structures.

Disadvantages:

- Unlimited liability for the general partner. Without an LLC acting as the general partner, the individual managing the LP faces personal financial exposure for all business debts and claims.

- Illiquid partnership interests. Transferring LP interests usually requires unanimous consent, and interests are generally not designed for quick resale. This limits exit flexibility for both general and limited partners.

- Management concentration risk. All operational authority rests with the general partner. If that partner makes poor decisions or faces personal legal issues, the entire partnership is affected.

- Administrative complexity. LPs require state filings, annual compliance, and a well-drafted partnership agreement. The administrative burden is higher than a simple general partnership.

The illiquidity point deserves emphasis. LP interests are not publicly traded shares. An investor who wants to exit typically cannot do so without the consent of the other partners, which makes LP investments a long-term commitment. Entrepreneurs raising capital through an LP structure should communicate this clearly to prospective investors before they sign.

What are the steps to form a limited partnership?

Forming an LP is a state-level process with specific legal requirements that vary by jurisdiction.

- Choose your state of formation. Delaware and California are the most common states for LP formation due to well-developed partnership law and predictable court interpretations. Delaware's Court of Chancery has extensive LP case law, which provides legal clarity.

- File a certificate of limited partnership. This document is filed with the Secretary of State and establishes the LP under the state's Uniform Limited Partnership Act. It typically includes the LP's name, principal address, and the name of the registered agent.

- Draft a limited partnership agreement. This is the most critical document in the formation process. A comprehensive partnership agreement defines partner roles, profit-sharing formulas, voting rights, admission of new partners, and dissolution procedures. Without it, state default rules govern the partnership, which rarely match the parties' intentions.

- Designate a registered agent. Every LP must have a registered agent in the state of formation to receive legal notices and official correspondence.

- Obtain an EIN. The IRS requires an Employer Identification Number for the LP to file taxes, open bank accounts, and hire employees.

- Complete annual filings. Most states require annual or biennial reports to maintain the LP's good standing. Missing these filings can result in administrative dissolution and loss of liability protections.

Pro Tip: If you plan to operate in multiple states, register the LP as a foreign limited partnership in each state where you conduct business. Failing to do so can expose the general partner to penalties and strip the LP of its legal protections in those states.

For entrepreneurs who want to protect the general partner from personal liability, forming a California LLC or another state LLC to serve as the general partner is a practical step. Legalstepz covers the LLC formation process in detail for entrepreneurs considering this layered structure.

Staying current on annual compliance requirements is equally important after formation. Good standing is not automatic. It requires consistent attention to state deadlines and reporting obligations.

Key takeaways

A limited partnership gives entrepreneurs a legally defined structure to separate management control from passive investment, with pass-through taxation and scalable capital-raising potential.

| Point | Details |

|---|---|

| Two-class partner structure | General partners manage and bear unlimited liability; limited partners invest and stay passive. |

| Pass-through tax treatment | Profits and losses flow to individual returns, avoiding double taxation at the entity level. |

| Liability risk for active limited partners | Courts can reclassify limited partners as general partners if they participate in management. |

| LLC as general partner | Forming an LLC to serve as general partner shields individuals from unlimited personal liability. |

| Illiquid interests | LP interests require unanimous consent to transfer, making them a long-term capital commitment. |

Why I think most entrepreneurs underestimate the general partner liability problem

Most articles on limited partnerships spend three paragraphs on tax benefits and one sentence on general partner liability. That ratio is backwards. In my experience working with entrepreneurs on business formation, the unlimited liability exposure of the general partner is the single most consequential feature of the LP structure, and it is the one most often glossed over in the excitement of raising capital.

The LLC-as-general-partner strategy is not a loophole or an advanced technique. It is the standard approach for any LP where the stakes are meaningful. If you are forming an LP to syndicate real estate or run a private fund, and you are not using an LLC as the general partner, you are accepting personal liability for every deal the partnership makes. That is a structural choice, not an oversight, and it should be a deliberate one.

The other issue I see repeatedly is limited partners who drift into management. It usually starts small. An investor asks to review a vendor contract. Then they start attending operational meetings. Then they weigh in on hiring decisions. Each step feels minor, but collectively they can trigger reclassification under state law. The partnership agreement needs to define safe harbor activities in writing, and the general partner needs to enforce those boundaries consistently.

LPs are genuinely powerful structures for the right use cases. Real estate syndications, private equity vehicles, and family investment partnerships all benefit from the clean separation of management and capital. But that power comes with legal precision requirements that general partnerships and LLCs simply do not have. Treat the formation documents as the foundation, not the paperwork.

— Peter

How Legalstepz can help you form your limited partnership

Forming a limited partnership involves more moving parts than most entrepreneurs expect, from state filings and registered agent designations to drafting a partnership agreement that actually protects everyone involved. Legalstepz is built to guide you through each step without the confusion.

Whether you are starting from scratch or trying to understand what your existing structure requires, the Legalstepz Incorporation Course walks you through business entity formation with the legal clarity you need to make confident decisions. For entrepreneurs who want hands-on document support, business formation assistance is available to handle LP filings, partnership agreements, and registered agent services. Visit Legalstepz to explore the full range of formation and compliance tools built for business owners at every stage.

FAQ

What is the limited partnership definition in simple terms?

A limited partnership is a business entity with at least one general partner who manages the business and bears unlimited liability, and at least one limited partner whose liability is capped at their capital contribution.

What does a limited partner actually do?

A limited partner contributes capital and receives a share of profits but takes no role in day-to-day management. Participating in operations beyond defined safe harbor activities risks reclassification as a general partner under state law.

How does a limited partnership differ from an LLP?

A limited liability partnership grants limited liability to all partners, including those who manage the business. A limited partnership requires at least one general partner with unlimited personal liability, which is the fundamental structural difference between the two.

What are the main tax implications of a limited partnership?

LPs are pass-through entities, so profits and losses are reported on each partner's individual tax return. Limited partners are generally exempt from self-employment taxes unless they actively participate in management beyond their investment role.

How do you form a limited partnership?

File a certificate of limited partnership with your state's Secretary of State, draft a comprehensive limited partnership agreement, appoint a registered agent, and obtain an EIN from the IRS. Annual filings are required in most states to maintain good standing.